HCF health insurance is one of the largest and most established private health funds in Australia, offering a wide range of hospital and extras cover for singles, couples, and families. Known for its not-for-profit structure, HCF reinvests profits into member benefits rather than shareholders, and has built a strong network of participating providers across the country.

With over 1.9 million members, HCF is often considered for its family-friendly policies, gap cover arrangements, and access to health and wellbeing services. However, the real value depends on the specific policy you choose, as costs, inclusions, and out-of-pocket expenses can vary widely.

This guide looks at what HCF health insurance includes, how its cover works, pricing, benefits, and the key pros and cons to help you understand whether it suits your needs.

HCF at a Glance

| Feature | Details |

|---|---|

| Founded | 1932 |

| Members | 1.9+ million |

| Fund Type | Not-for-profit |

| Policies | Hospital, Extras, Combined |

| Mobile App | Yes |

| Ambulance Cover | Included in most policies |

| Adult Dependants | Up to age 31 |

| Gap Cover Program | Yes |

| Rewards Program | Yes |

What Is HCF?

HCF (Hospitals Contribution Fund of Australia) is Australia’s largest not-for-profit health insurer.

Unlike for-profit insurers, HCF reinvests profits back into member services, benefits, and health programs rather than paying shareholders. That structure appeals to Australians who want value-focused cover instead of investor-driven pricing.

Today, HCF covers singles, couples, families, retirees, and young adults through a broad range of hospital and extras policies.

What Makes HCF Different?

HCF stands out in several areas where many competing funds are fairly similar.

Strong Family Cover

HCF is particularly generous with dependant rules.

- Children are covered free on family policies until age 22

- Full-time students can remain covered until age 31

- Extended family cover is available for some adult dependants

That makes HCF more family-friendly than many competitors.

Large No-Gap Provider Network

HCF has a large network of participating dentists, optical providers, and medical specialists.

Eligible members may receive:

- no-gap dental

- reduced optical costs

- lower out-of-pocket hospital expenses

This can significantly improve value if you regularly use extras services.

Not-for-Profit Model

Many Australians specifically prefer not-for-profit insurers because profits are reinvested into:

- member benefits

- health programs

- digital tools

- provider networks

While this does not automatically mean cheaper premiums, it often improves perceived value.

Types of HCF Cover

Hospital Cover

Hospital cover helps pay for treatment as a private patient in hospital.

Depending on your policy tier, cover may include:

- joint replacements

- pregnancy and birth

- heart procedures

- cataracts

- mental health treatment

- cancer care

HCF offers:

- Basic

- Bronze

- Silver

- Gold

- Plus-tier products

Best For

People wanting:

- shorter public waiting times

- private rooms (where available)

- choice of doctor

Extras Cover

Extras cover helps pay for services Medicare usually does not cover.

Common inclusions:

- dental

- optical

- physiotherapy

- psychology

- podiatry

- chiropractic

- speech therapy

HCF’s extras network is one of its strongest selling points because participating providers can reduce or eliminate out-of-pocket costs.

Combined Cover

Combined policies bundle hospital and extras into one policy.

This is generally the best option for:

- families

- regular dental users

- people wanting broader protection

HCF Gap Cover Explained

One of the biggest hidden costs in private health insurance is the medical gap.

This is the difference between:

- what Medicare pays

- what your specialist actually charges

HCF’s gap cover system aims to reduce these surprise expenses through agreements with participating doctors.

There are two common arrangements:

| Type | What You Pay |

|---|---|

| No Gap | $0 |

| Known Gap | Capped fee |

- If your doctor participates in HCF’s program, out-of-pocket costs can be dramatically lower.

- However, not every specialist participates, which is an important limitation many consumers overlook.

HCF Complaints and Customer Experience

HCF generally performs around the industry average for complaints relative to its size.

Common positive feedback includes:

- easy digital claiming

- large provider network

- useful extras cover

- family-friendly policies

Common complaints include:

- annual premium increases

- confusion around policy exclusions

- occasional claim processing delays

Compared with budget insurers, HCF is usually seen as more established and service-oriented, though not necessarily the cheapest.

Is HCF Good Value?

HCF delivers the best value for people who actually use their cover regularly.

It can be particularly worthwhile if you:

- claim dental often

- need optical benefits

- have children on family cover

- prefer private hospitals

- use participating providers

For low-usage members who mainly want the cheapest premium, smaller budget funds may offer lower-cost alternatives.

HCF Pricing: What Does It Cost?

Premiums vary based on:

- age

- location

- income

- cover level

- excess amount

Typical ranges are roughly:

| Policy Type | Approx Monthly Cost |

|---|---|

| Basic Hospital | AU$25–50 |

| Mid-Tier Hospital | AU$80–150 |

| Comprehensive Combined Cover | AU$150–300+ |

- Prices vary significantly by state and rebate eligibility.

- One weakness of HCF is that its stronger extras and provider benefits can come with higher premiums than some low-cost competitors.

Ambulance Cover

Most HCF hospital, extras, and combined policies include emergency ambulance cover.

However, ambulance arrangements vary between Australian states, so the exact level of cover depends on:

- your state

- your policy

- local ambulance schemes

This is important because ambulance transport can be extremely expensive without cover.

HCF App and Claims Experience

HCF’s digital experience is better than many older health funds.

The HCF app allows members to:

- submit claims

- track limits

- manage policies

- estimate benefits

- access digital membership cards

Many extras claims process quickly through participating providers.

The app is convenient, though some users still report occasional delays during peak periods.

HCF Pros and Cons

Pros

- Largest not-for-profit health fund in Australia

- Strong family cover options

- Large participating provider network

- Good extras value for regular users

- Convenient mobile app

- Wellness and telehealth programs

- Adult dependants covered up to 31

Cons

Premiums can be expensive

Lower-tier extras policies may feel restrictive

Some benefits require participating providers

Waiting periods still apply

Not always the cheapest option for young singles

HCF vs Other Health Funds

| Feature | HCF | Bupa | Medibank | nib |

|---|---|---|---|---|

| Not-for-Profit | Yes | No | No | No |

| Strong Family Cover | Excellent | Moderate | Moderate | Moderate |

| Provider Network | Large | Large | Large | Large |

| Rewards Program | Yes | Yes | Yes | Yes |

| Adult Dependants to 31 | Yes | Limited | Limited | Limited |

HCF’s strongest advantage is its balance between:

- family value

- extras benefits

- not-for-profit positioning

Its weakest point is pricing competitiveness against leaner budget funds.

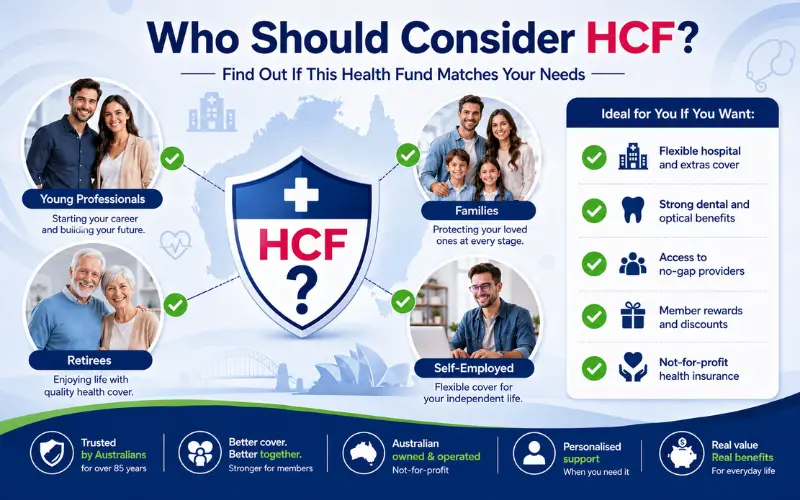

Who Should Consider HCF?

HCF is a strong fit for:

- families with adult children

- frequent dental users

- people wanting extras value

- Australians who prefer not-for-profit insurers

- members who regularly claim health services

Who Might Prefer Another Fund?

You may prefer another insurer if:

- you only want the cheapest possible premium

- you rarely use extras

- your preferred providers are outside HCF’s network

- you want ultra-basic cover with minimal features

FAQs

Is HCF health insurance a good choice for families?

HCF health insurance is a popular option for families because it allows eligible adult children to stay on a family policy until age 31 in some circumstances. It also offers cover for common extras such as dental, optical, and physiotherapy, along with access to member rewards and health programs that can provide additional value for households.

What does HCF health insurance cover?

HCF health insurance offers hospital cover, extras cover, and combined policies. Depending on the level of cover you choose, benefits may include private hospital treatment, ambulance services, dental care, optical benefits, physiotherapy, chiropractic treatment, and other services that Medicare does not usually cover.

Does HCF health insurance include ambulance cover?

Most HCF health insurance policies include emergency ambulance cover, but the exact benefits can vary based on your policy and the state where you live. This cover can help protect you from high ambulance costs if you need urgent medical transport.

How long are the waiting periods for HCF health insurance?

HCF health insurance waiting periods are similar to those offered by other Australian health funds. General extras often have a two-month waiting period, while major dental, pregnancy, and pre-existing conditions may have waiting periods of up to 12 months.

How do you make a claim with HCF health insurance?

You can make a claim with HCF health insurance through the HCF My Membership app, the online member portal, at an HCF branch, or directly at participating providers. Many extras claims are processed instantly, making the claiming process quick and convenient.

Is HCF health insurance worth it?

HCF health insurance can be worth it if you want a not-for-profit health fund with a long history, a large provider network, and valuable member benefits. Many Australians choose HCF for its strong family features, no-gap options, and access to discounts and health support programs.

Final Verdict

HCF remains one of Australia’s strongest all-round health insurers.

Its biggest strengths are:

- family-friendly policies

- broad provider network

- strong extras benefits

- not-for-profit structure

- mature digital experience

It is not the cheapest health fund on the market, and lower-usage members may find better value elsewhere. But for Australians who regularly use dental, optical, or hospital services, HCF can offer very solid long-term value.

Overall, HCF is best suited to members who want reliable coverage, strong extras support, and a health fund focused more on member benefits than shareholder profit.